Why Cyber Insurance Claims Are Denied: 5 Reasons Brokers See

Cyber insurance exists to protect you when the worst happens, yet carriers deny more claims than most brokers expect. According to Market.us, 27% of data breach claims had policy exclusions that reduced or denied payment..The problem isn’t always a technicality buried in fine print. It’s often something you could’ve caught before your client ever filed. Five specific patterns show up repeatedly why cyber insurance claims are denied,and understanding them changes how you approach every policy you write.

Key Takeaways

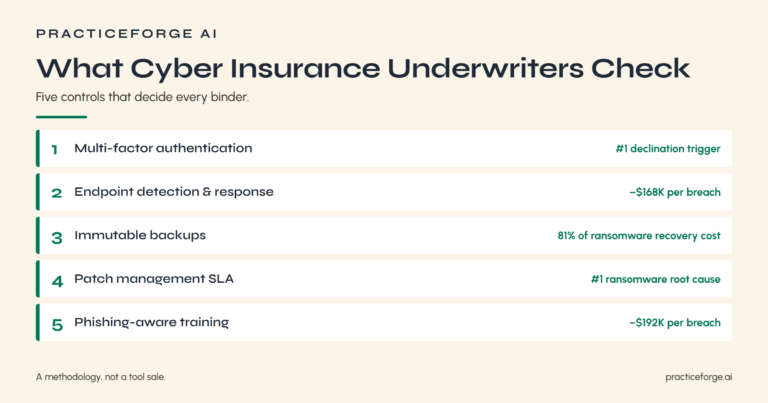

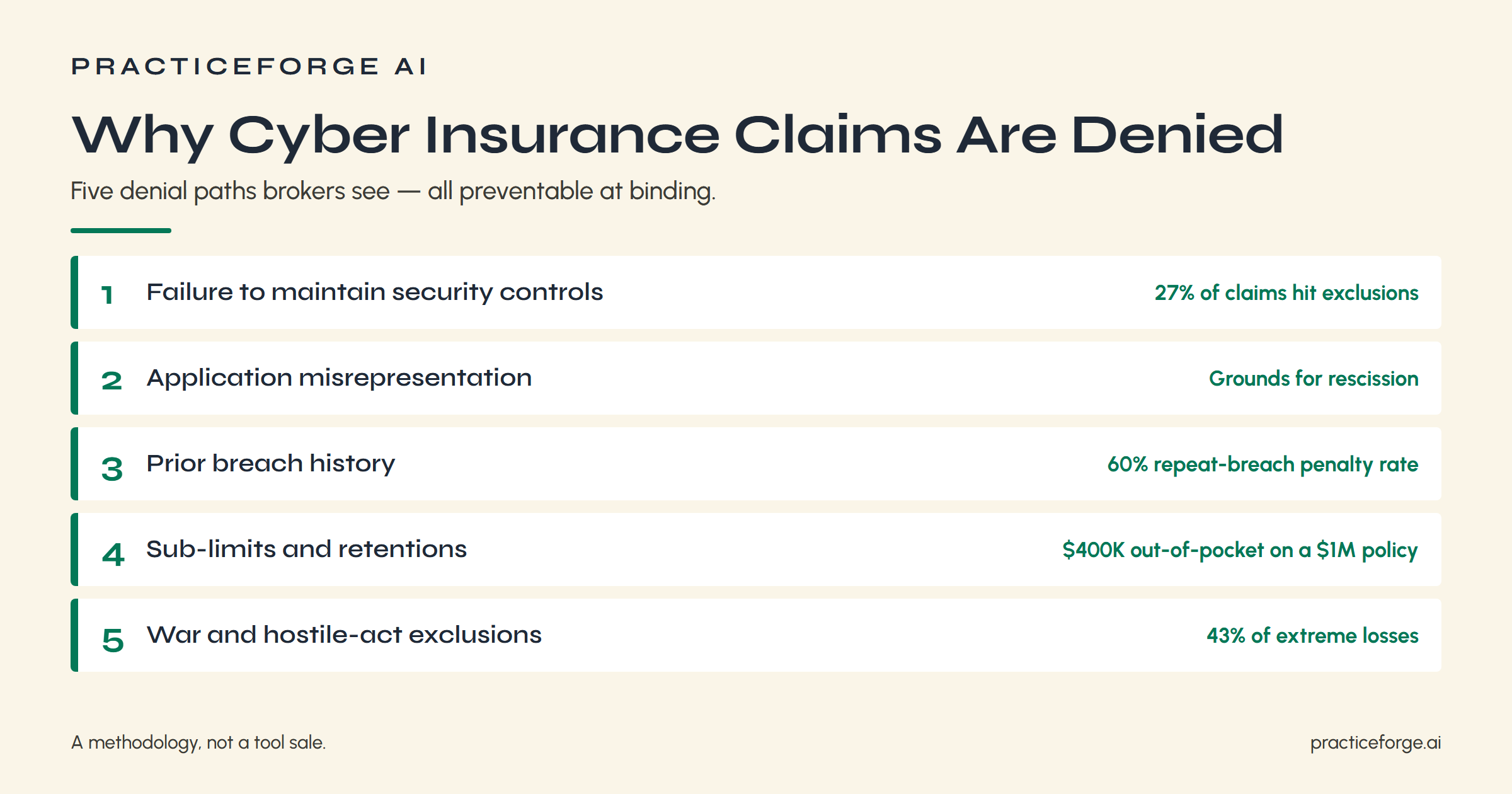

- Security control failures void coverage. Lapsed MFA, unpatched systems, and missing EDR are the most common “failure to maintain security exclusion triggers. They are the first thing the adjuster checks.

- Application misrepresentation gives carriers grounds for recission. If the controls you said were in place aren’t actually deployed, the claim doesn’t pay. This is true regardless of how legitimate the loss is.

- Prior breach history kills renewals. 60% of organizations that breached more than once faced penalty pricing, sub-limit aggression, or non-renewal. Undocumented remediation makes it worse.

- Sub-limits and retentions gut payouts. A $1M aggregate doesn’t mean $1M for ransomware. Sub-limits cap specific loss categories, and per-claim retentions compound across coverage modules.

- War and hostile-act exclusions follow state-linked attacks. Cyentia shows 43% of extreme event cyber losses trace to state-affiliated actors. Attribution doesn’t require certainty, just plausibility.

1. Security Control Failures That Void Cyber Insurance Coverage

When a cyber claim lands on a carrier’s desk, the first thing the adjuster checks isn’t the breach details.

It’s whether your client had the controls the application said they had.

Understanding the most common control gaps., How to screen for them before binding is where you protect both your client and your book.

Common Control Gaps

Most cyber insurance claims don’t happen because the attack was unforeseeable. They happen because the business wasn’t doing what the policy required.

These are the common control gaps that turn covered incidents into denied claims:

- MFA not implemented across remote access and email, despite being listed as a policy requirement

- Unpatched systems left exposed to known CVEs, violating reasonable security measures standards

- No employee training on phishing or social engineering, which directly contributes to the breach

- Missing or untested incident response plans, making it impossible to prove compliance after the fact

- Unvetted third-party vendors introducing vulnerabilities the carrier never agreed to cover

- Per the Sophos State of Ransomware, exploited vulnerabilities are the #1 root cause of ransomware attacks — and unpatched systems are a common basis

Each gap chips away at the financial protection your client thought they had.

Security controls on paper don’t count. They’ve to be operational.

Broker Pre-Screening Steps

Knowing the control gaps is useful. Acting on them before a client submits an application is what actually prevents cyber insurance claims from getting denied. During the underwriting process, run three pre-screening checks before binding:

- Confirm security controls are active and documented. Missing evidence triggers automatic denial.

- Verify compliance with security requirements: MFA, patching cadence, EDR deployment.

- Review policy exclusions against the client’s actual environment so cyber incidents don’t hit a coverage wall at claim time.

Documentation isn’t optional. Carriers treat undocumented controls as nonexistent controls.

Build timely communication protocols into your client onboarding so incident reporting deadlines don’t get missed post-breach. Pre-screening shifts your role from policy deliverer to coverage guarantor. That’s the difference between a claim that pays and one that doesn’t.

If you want the actual list of controls underwriters check before binding, the free cyber-readiness assessment covers it client-by-client, in plain language, with no login required.

2. Application Misrepresentation: The Denial Carriers Find First

When a carrier investigates a claim, the application is the first document they pull.

If the controls you said were in place aren’t actually deployed, that gap isn’t an oversight, it’s grounds for rescission.

Understanding what misrepresentation looks like, and how to correct it before binding, is where you protect your client from a denial that was baked in before the policy ever incepted.

What Misrepresentation Looks Like

Nobody sets out to commit insurance fraud. But misrepresentation in cyber insurance claims doesn’t require intent. It just requires a discrepancy between what your application says and what claims investigation confirms.

Common examples carriers find during claims processing:

- Multi-Factor Authentication listed as active on the application but not enforced across email or remote access at the time of loss

- Endpoint protection checked “yes” on the form but deployed inconsistently across workstations

- Third-party vendors with system access never disclosed during underwriting

Underwriters treat applications as legal documents. When cybersecurity measures don’t match what you reported, carriers have grounds to deny, regardless of how legitimate the loss is.

Accurate applications aren’t just good practice. They’re what preserves your client’s insurance eligibility when it matters most.

Fixing It Before Binding

The fix isn’t complicated, but it has to happen before you bind the policy.

Walk your client through every security control listed on the application. Don’t ask if they’ve MFA. Ask how it’s enforced, where it’s deployed, and who audits compliance. Cyber insurance claim denials tied to misrepresentation aren’t always intentional. Clients overstate their cybersecurity posture because they believe partial implementation counts. It doesn’t.

Run a pre-submission review against the carrier’s insurance requirements. Treat it like a mini risk assessment.

Compare actual security measures against what the application process will capture. If the security controls aren’t fully operational, document what’s in progress and disclose it. Underwriting can price around gaps. It can’t price around misrepresentation discovered at claim time.

3. How Prior Breach History Kills Cyber Insurance Claims and Renewals

If your client has a prior breach on record, the underwriter already knows it before the submission hits their desk. (This is where cyber-insurance broker automation pre-screening pays off. Surface the prior breach before the carrier does.)

Carriers don’t treat past incidents as water under the bridge; they treat them as predictive data, and they’ll price accordingly, sub-limit aggressively, or decline to renew.

Your job is to close the controls gap that the prior breach exposed and document every remediation step before the next renewal conversation starts.

Repeat Claims Carrier Penalties

When a client has been breached before, carriers don’t start the underwriting conversation at zero. Insurers expect a documented improvement in security posture, and if your client can’t show it, you’ll see it priced into the renewal or denied outright.

Repeat claims signal inadequate cybersecurity controls, and carriers treat that pattern as predictive, not coincidental.

Here’s what repeat breach history triggers:

- Premium increases or non-renewal, reducing the financial response options your client actually has

- Stricter underwriting criteria that narrow coverage terms and reasons for claim denials

- Heightened scrutiny over accuracy or completeness of the application, including whether an incident response plan exists

Cyber insurance provides coverage assuming baseline controls held. Repeat claims tell carriers they didn’t.

Controls Gap Documentation

Carriers don’t take your word for it that controls were in place. When cyber insurance claims get investigated, insurers require documented proof that your client’s security controls were active at the time of loss.

Per the NAIC 2024 Cyber Insurance Report, carriers require documented proof that security controls were active at the time of loss.

MFA logs. Patch records. Endpoint detection reports. If those records don’t exist, the claim denial follows almost automatically.

Breach history compounds the problem. Carriers scrutinize prior ransomware attacks and incidents for gaps in documentation. Inaccurate or incomplete records of past breaches, response timelines, and resolutions signal that security measures weren’t taken seriously.

Your client also needs a current, written incident response plan. Insurers treat the absence of one as evidence of inadequate preparation.

Accuracy matters here. Documentation isn’t a formality. It’s the evidentiary foundation that determines whether the policy pays.

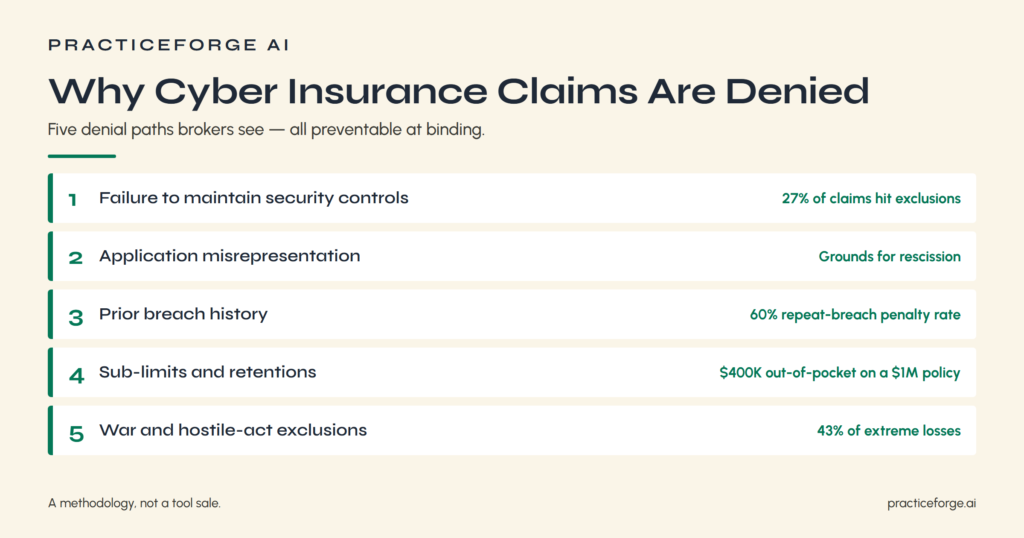

4. Sub-Limits and Retentions That Gut Payouts Before Settlement

You can bind a policy with a $1M aggregate limit and still watch your client absorb $400K out of pocket because the ransomware sub-limit caps at $250K and the retention runs another $150K before the carrier pays a dollar.

Most SME cyber policies are structured this way, and the client never sees it until the claim hits.

That’s not a coverage gap you find at settlement; it’s one you find at the application stage, if you know where to look.

How Sub-Limits Slash Payouts

The policy limit your client sees on the declarations page isn’t what they’ll collect after a breach. Insurers structure cyber insurance policies with sub-limits that cap payouts on specific loss categories well below the overall coverage amount.

A $1M policy might carry:

- $100K sub-limit on ransomware payments

- $250K sub-limit on business interruption losses

- $50K sub-limit on regulatory fines from data breaches

Those figures don’t stack toward the main limit. They replace it for those claim categories.

When actual losses hit $485K across crisis response, legal, and direct costs, sub-limits turn adequate-looking coverage into a financial recovery shortfall. Your client faces unexpected expenses no one discussed at binding.

Pull the declarations and endorsements before renewal, not after the claim lands on your desk.

Retention Gaps Brokers Miss

Retention is where a lot of cyber policies quietly fall apart. Your client paid the premium, the carrier accepted the claim, and then the retention kicks in and swallows a number nobody planned for.

Many businesses assume their retention works like a standard commercial deductible. It doesn’t. Cyber retentions often apply per-claim event, and some policies layer separate retentions across coverage parts.

That means your client could face compounding out-of-pocket costs across crisis response, legal, and recovery efforts before the policy limits pay anything.

When you’re reviewing coverage details at binding, ask specifically how retention applies across each coverage module.

Retention gaps are one of the quieter reasons claims denied outcomes happen. Brokers who surface this early give clients time to fund it properly.

5. War and Hostile-Act Exclusions That Follow State-Linked Attacks

When NotPetya swept through global networks in 2017, carriers denied hundreds of millions in claims by invoking war and hostile-act exclusions, arguing the attack was a Russian military operation against Ukraine.

Zurich American’s denial of Mondelez’s $100M claim became the most visible test case, and courts took years to sort out whether a cyberattack attributed to a nation-state qualifies as an “act of war” under a commercial property policy.

That ambiguity didn’t disappear when the Mondelez case settled quietly in 2022. It migrated directly into cyber policy language, where 43% of extreme-event cyber losses now trace back to state-affiliated actors, according to Cyentia IRIS Xtreme data.

NotPetya’s Denied Claims

Reason three is the one that blindsides even experienced brokers: war and hostile-act exclusions.

NotPetya demonstrated exactly how denied claims happen when state-sponsored attacks trigger policy exclusions businesses never saw coming. Carriers classified NotPetya as a hostile act, voiding coverage for billions in losses. Policies excluded it. Businesses paid out of pocket.

What your clients need to understand before binding:

- War exclusions don’t require a formal declaration of war. State-affiliated attribution is enough.

- NotPetya caused $3.5B in losses. Cyentia data shows 43% of extreme-event cyber losses trace to state-affiliated actors.

- Understanding your policy language around “hostile acts” isn’t optional. It’s the difference between a paid claim and a denied one.

Ask your carrier directly: how do they define state-sponsored cyber threats?

State-Actor Attribution Gaps

The part that catches most brokers off guard isn’t the exclusion itself. It’s that establishing attribution for cyber attacks is genuinely hard, and carriers know it. When a cyber insurance policy includes war exclusions, the insurer doesn’t need a declaration of war. They need enough technical evidence to argue state-sponsored attacks were involved. That’s a low bar when incident analysis is incomplete.

Your client’s documentation and evidence have to address origin, not just damage. If the insurer can point to known state-affiliated infrastructure, claims denied becomes the likely outcome.

Policy exclusions tied to hostile acts don’t require certainty, only plausibility. That gap between what happened and what’s provable is where insurance coverage disappears. Build the documentation requirement into the reporting protocol before a cyber incident occurs.

Frequently Asked Questions

What Are 5 Reasons a Claim May Be Denied?

Your client’s cyber claim can get denied for five reasons: failed security controls, sub-limits below actual loss, war exclusions, repeat-breach history, and application misrepresentation about controls that weren’t actually in place.

What Are the Common Exclusions in Cyber Insurance Policies?

You’ll commonly see exclusions for war/hostile acts, failure to maintain security controls, prior breaches, unencrypted data losses, wire transfer fraud, and physical damages. Each can void coverage your client assumes they have.

What Not to Say to the Insurance Adjuster?

Don’t admit fault, speculate on causes, or guess at your security controls’ status. Stick to documented facts, avoid vague language, and never assume your coverage applies without confirming specific policy terms first.

What Causes Most Cybersecurity Breaches?

Per the IBM Cost of a Data Breach Report (2025), the root cause split is 51% malicious attacks, 26% human error, and 23% IT failure. That means roughly half are attacker-driven and half are operational – training, patching and access controls address most of what’s inside the broker’s control Don’t bind a policy without verifying the client has all three.

Conclusion

Claim denials aren’t carrier cruelty. They’re a controls-and-policy-language problem brokers can solve at binding. The same audit-before-build approach that drives our methodology.,

Every reason on this list is documented in carrier data, predictable at the application stage, and screenable before the policy incepts. The brokers who win renewals are the ones doing that screening before the underwriter does.

Pre-screen your next client against the controls underwriters actually check

The free cyber-readiness assessment walks your client through the MFA, EDR, patching, backup, and incident-response questions that determine whether a policy pays. Built for the 1–20-agent brokerage. No login required.

Or book a 20-minute call to walk through your book of business.

Michael Toback is the founder of PracticeForge AI. Licensed California P&C agent (#4528883), retired California Bar and USPTO patent attorney, CompTIA CySA+, ACRM 401 Cyber Risk Management. More about Mike →