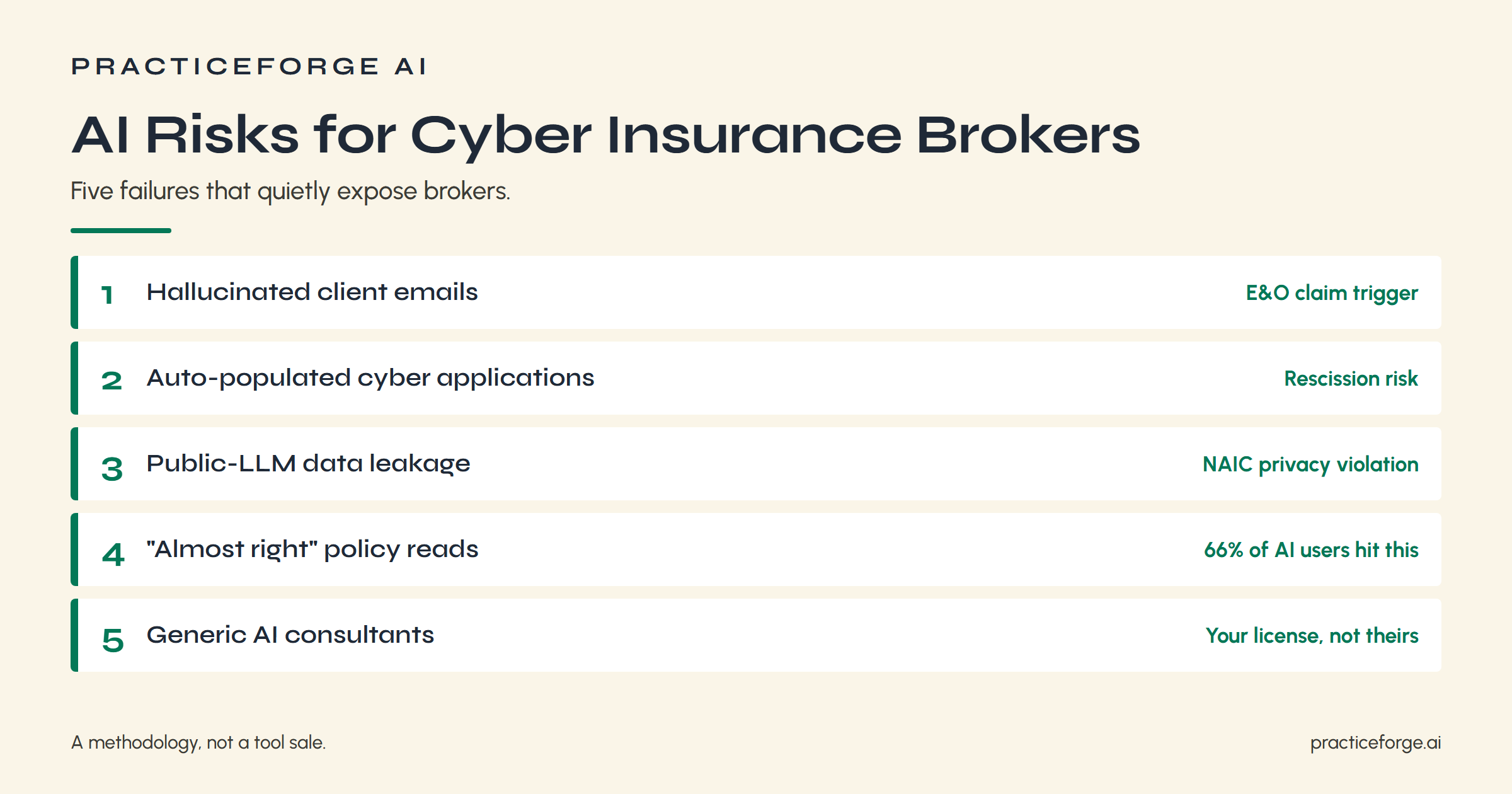

AI Risks for Cyber Insurance Brokers: 5 Failures to Avoid

You don’t have to abandon AI tools to protect yourself from liability. You just need to know where they fail. From hallucinated policy details in client emails to misread exclusions that blindside you at claim time, the risks are specific and preventable. Five critical AI risks for cyber insurance brokers are quietly exposing them right now. Understanding each one could be the difference between a thriving practice and an E&O nightmare.

The numbers say the worry is justified. RAND Corporation and McKinsey both peg AI project failure rates at 80%. Only 12% of CEOs say AI has delivered both cost and revenue benefits, and 56% report no benefit at all, per the PwC 2026 Global CEO Survey. For a licensed cyber-insurance broker, those failures aren’t abstract. They land as E&O claims, application rescissions, and state DOI inquiries.

Key Takeaways

- AI hallucinations can cause brokers to relay incorrect coverage details, triggering E&O claims when clients suffer uninsured losses.

- AI-generated cyber applications may misrepresent client controls like MFA, creating warranty breaches that void coverage at claim time.

- Pasting client data into unsecured AI tools risks privacy violations, exposing brokers to regulatory penalties and licensing consequences.

- AI routinely misreads policy exclusions and omits sub-limits, leaving clients with false expectations about their actual coverage scope.

- All AI-assisted outputs require human sign-off, verified client data, and consultant vetting aligned with ACORD and NAIC obligations.

1. AI Hallucinations in Client Emails That Trigger Cyber E&O Claims

You ask your AI tool whether a client’s cyber policy covers ransomware. It tells you yes, and you forward that answer in an email without checking the sub-limit buried in the endorsement.

That single exchange—AI drafts it, you send it, client relies on it—is a textbook E&O trigger the moment the carrier caps the ransomware payout at $100,000 on a $2 million loss.

When AI confidently lies about coverage, the license on the line is yours, not the chatbot’s.

When AI Confidently Lies

Imagine this: a client emails you on a Friday afternoon asking whether their new cyber policy covers a ransomware attack on their cloud storage vendor.

You’re juggling three renewals, so you paste the policy into ChatGPT and ask. The AI confidently says yes. You forward that answer.

What the AI missed: a $100,000 sub-limit buried in the contingent business interruption clause that caps vendor-related losses well below your client’s actual exposure.

That’s not a technology glitch. That’s an E&O liability trigger.

AI trustworthiness isn’t guaranteed. Only 29% of developers trust AI outputs as accurate (down from 40% in 2024), per Stack Overflow’s 2025 Developer Survey.

In client communication, “almost right” isn’t right. Your application accuracy, risk management obligations, and data privacy duties don’t pause because the AI sounded confident.

Your E&O Exposure Explained

The Friday-afternoon scenario isn’t hypothetical. It’s the exact fact pattern that generates E&O claims against brokers. You forwarded an AI-generated coverage answer without running coverage validation against the actual policy language. Your client relied on it. The claim got denied. Now you own the gap.

Your E&O strategies have to account for where AI sits in your workflow. That means building AI audits into your file documentation, treating every AI-assisted coverage summary as requiring human sign-off, and folding liability management into your client education conversations upfront.

Regulatory compliance adds another layer — state DOI standards don’t bend because your AMS plug-in generated the answer. Risk assessments, data privacy obligations, and carrier relationships all connect here.

The AI didn’t make the representation. You did.

2. How AI-Drafted Cyber Applications Create Warranty Misrepresentation

You’ve seen the demo: paste the client’s IT questionnaire into an AI tool, and it spits out a completed cyber application in minutes.

The problem is that the AI doesn’t know what controls your client actually has. It knows what a well-secured company *should* have, and it fills in the blanks accordingly.

When that application becomes a warranty at binding and the client suffers a breach, those plausible-but-unverified answers about the five controls underwriters actually check become the carrier’s rescission argument..

The Auto-Population Trap

When a broker asks an AI tool to help fill out a cyber application, the tool does exactly what it’s built to do: generate confident, plausible-sounding answers. The problem? Those answers reflect training data, not your client’s actual security protocols.

| AI-Generated Answer | What It Assumes | The Real Risk |

|---|---|---|

| “MFA enabled across all systems” | Universal deployment | Partial rollout triggers exclusion |

| “Daily encrypted backups confirmed” | Client verification exists | No data integrity checks were run |

| “EDR deployed enterprise-wide” | Full endpoint coverage | Legacy systems left unprotected |

| “Patch cycle: 30 days or fewer” | Documented verification mechanisms | Informal process, unverifiable at claim |

| “Incident response plan in place” | Formal documented policy | Verbal procedure, no client consent trail |

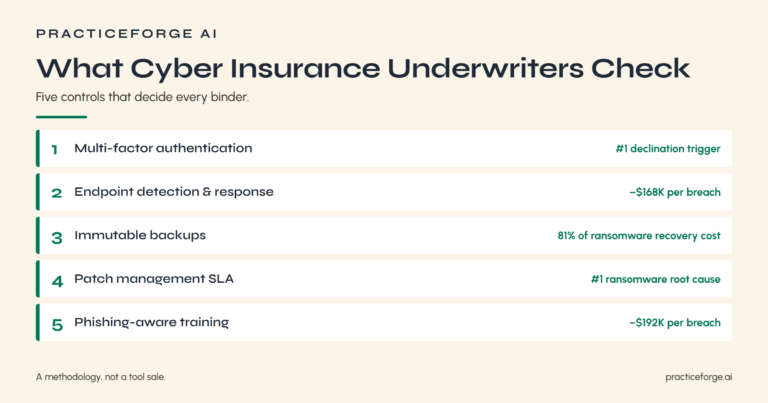

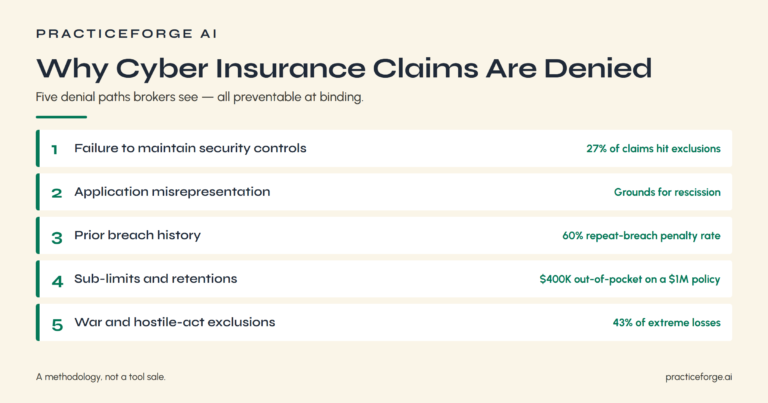

This isn’t theoretical. Market.us data shows 27% of cyber claims hit policy exclusions that reduced or denied payment. Per the NAIC 2024 Cyber Insurance Report, “failure to maintain security” exclusions and application misrepresentation are the two mechanisms carriers use most often to rescind. Auto-populated answers don’t survive a denial investigation. The misrepresentation lands on you.

Fixing the Verification Gap

Knowing the auto-population trap exists is only half the fix. You need verification methods that close the gap before the application becomes a warranty.

Build a client communication checkpoint: every AI-drafted control answer goes back to the client’s IT contact for written confirmation before submission. That paper trail is your misrepresentation risk shield at claim time.

For data validation, cross-reference AI interpretation against your own coverage assessment notes and the carrier’s specific control definitions. They’re not interchangeable.

“MFA enabled” means different things to ChatGPT and a cyber underwriter.

On privacy compliance, never paste security posture data into a public LLM to speed up the review.

Risk mitigation here is simple: AI drafts, humans verify, clients sign off. In that order. Every time.

3. Why Pasting Client Security Data Into ChatGPT Breaks DOI Privacy Rules

When you paste a client’s cyber application, breach narrative, or security assessment into ChatGPT or Claude, you’re sending more than text. You’re transmitting MFA configurations, network architecture details, prior breach history, and account credentials into a public model’s infrastructure you don’t control.

That data doesn’t vanish after the session; depending on the platform’s retention settings, it can feed future model training or sit in logs accessible to the vendor.

State DOI privacy regulations and NAIC model rules treat that client security posture as nonpublic personal information, and the broker — not the AI vendor — owns the compliance violation when it leaks.

What Leaks When You Paste

The shortcut feels harmless: you’ve got a client’s completed cyber application in front of you, you paste it into ChatGPT to get a quick summary, and thirty seconds later you have clean, readable output.

But here’s what actually transferred with that paste:

- Security control gaps. (MFA exceptions, unpatched systems, backup failures now exist outside your control environment)

- Prior breach history. (Incident narratives that carriers treat as material underwriting facts)

- Client PII (Employee counts, revenue figures, named contacts, account identifiers)

Each item carries data privacy obligations, regulatory compliance exposure, and liability concerns your client never consented to.

Paste once, and you’ve compromised client trust, violated industry standards around underwriting integrity, and handed a public model information with serious ethical considerations attached.

AI limitations don’t excuse the breach.

The Regulatory Exposure Explained

Small-business concern about AI data privacy is the #1 adoption barrier — 38% of SMBs cite it as their top reason for hesitation, per the PayPal Beyond Efficiency Survey. For brokers, that concern translates into specific obligations: NAIC Model Regulation 672 on insurance information privacy, state-by-state DOI bulletins on AI use in underwriting (California, New York, Colorado, and Connecticut have all issued guidance through 2025), and the broker’s own producer license terms. None of these obligations defer to the AI vendor.

The compliance test isn’t “did the data leak?” It’s “could the broker prove, on the record, that client PII was processed only by tools the broker had authority to use?” Most public LLM usage in brokerages cannot pass that test today. The fix is enterprise tool selection (Microsoft Copilot for Business, Anthropic Claude with zero data retention, locally-hosted models), not user discipline.

If you’ve already pasted a client cyber application into a public LLM and you’re not sure what to do next, that conversation is worth having. Book a 20-minute call and walk through the cleanup steps.

4. The Policy Exclusion AI Misreads Before Your Client Files a Claim

You don’t need to be wrong by much to lose everything in a coverage dispute. You just need to be wrong at the one line that matters.

AI tools summarize cyber policies confidently, but that confidence doesn’t scale to the exclusion language underwriters actually use to deny claims.

If you’re not reading exclusions the way an underwriter would, you’re not reading the policy; you’re reading a paraphrase that could cost your client (and your E&O carrier) real money.

When “Almost Right” Costs Everything

Somewhere between “mostly accurate” and “exactly right” is where E&O claims are born. AI misinterpretation risks aren’t theoretical. Stack Overflow’s 2025 survey found 66% of developers frustrated by “almost right” outputs. For technical readers, “almost right” wastes time. For brokers, “almost right” generates E&O claims.

For brokers, “almost right” policy interpretation accuracy means a client binds coverage based on a flawed AI summary.

Watch for these three coverage clarity challenges:

- War exclusions misread as inapplicable when hostile-act language clearly triggers

- Sub-limits omitted from AI summaries, leaving clients assuming full-limit ransomware coverage

- Retroactive date gaps overlooked because the AI parsed the declarations page, not the conditions

Your regulatory liability factors don’t disappear because an algorithm made the call. Cyber insurance compliance demands broker AI proficiency and human verification—every time, before the client ever sees the answer.

Reading Exclusions Like Underwriters

When an underwriter reads a cyber policy exclusion, they’re not scanning for keywords—they’re reading for trigger conditions, defined terms, and the interaction between exclusion language and coverage grants.

You need that same discipline. Exclusion language nuances (“hostile act,” “governmental authority,” “failure to maintain”) carry liability threshold considerations that shift coverage dramatically based on one adjective.

AI misses these interactions because it pattern-matches, not reasons. That creates underwriting consistency challenges when you’re comparing quotes across carriers.

Your risk assessment implications multiply when a misread exclusion informs client communication strategies or shapes claims management procedures incorrectly.

For E&O mitigation tactics, build a checklist: every exclusion summary AI produces gets reviewed against the actual policy language. Privacy regulation compliance requires the same human verification discipline.

Own the read.

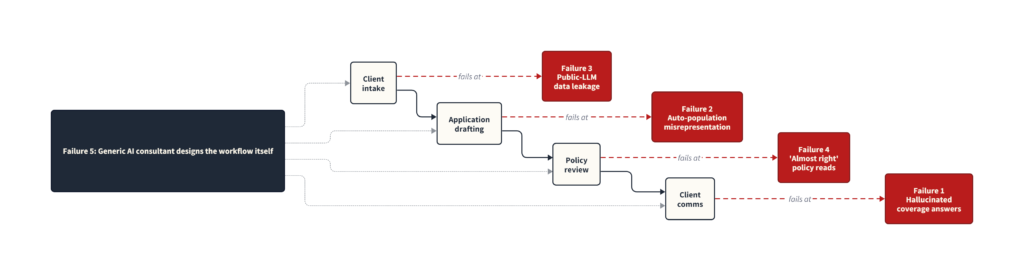

5. Generic AI Consultants: One of The Biggest AI Risks for Cyber Insurance Brokers

When you hire a generic AI consultant to build out your brokerage workflows, you’re handing your E&O exposure to someone who may never have read an ACORD form, touched a carrier portal agreement, or heard of a state DOI filing requirement.

The consultant ships the workflow, cashes the check, and walks away. Your producer license stays on the line when the build violates NAIC privacy obligations or scrapes data in ways your carrier agreements prohibit.

Understanding exactly where that regulatory blind spot sits, and why it lands on you instead of them, is what this failure mode is about.

The Regulatory Blind Spot

The consultant who built your AI intake workflow may be genuinely talented. They still have no idea that ACORD form licensing terms restrict how you can programmatically extract, reformat, or transmit standardized data fields.

That gap creates three distinct regulatory exposures you’ll own alone:

- ACORD licensing violations: automated field extraction without proper licensing triggers contractual liability, not just ethical considerations.

- State DOI marketing rules: AI-generated client communications may violate disclosure requirements your consultant never reviewed.

- NAIC privacy obligations: feeding applications into unsecured AI pipelines risks data breaches and regulatory compliance failures tied directly to your license.

Generic AI expertise doesn’t transfer to insurance innovation. Underwriting accuracy, data security, and AI limitations all require domain-specific oversight.

The brokerage signs the E&O policy. The consultant doesn’t.

Your License, Their Mistake

Hiring a generic AI consultant puts you in a specific legal position: you hold the license, you signed the carrier agreements, and you accepted the ACORD terms of service. Your consultant signed none of them. Their knowledge gaps become your compliance challenges. When their workflow violates DOI marketing rules or NAIC privacy obligations, the regulatory action lands on your E&O policy, not theirs.

| Their Mistake | Your Exposure |

|---|---|

| AI limitations ignored in automation | Data integrity failures at claim time |

| ACORD licensing violated | Contract breach with data partners |

| No verification protocols built in | Application misrepresentation risk |

| Ethical considerations skipped | State DOI regulatory action |

| Risk mitigation steps omitted | Carrier relationship terminated |

Vet every consultant against your specific regulatory compliance obligations before they touch a single client file.

Frequently Asked Questions

Does My E&O Policy Cover Losses Caused by Ai-Generated Advice?

Your E&O policy likely won’t cover AI-generated advice without clear liability assignments. Review your policy exclusions now, document AI limitations, obtain client consent, and guarantee compliance requirements are met before AI shapes your coverage clarity or risk assessment recommendations.

Can Carriers Void Coverage if AI Tools Accessed Our AMS Client Data?

Yes, in two specific scenarios. First, if the AI tool accessed AMS data in violation of your carrier portal terms of service or AMS vendor agreement, that’s contractual grounds to void or refuse renewal. Second, if the AI tool exposed client PII without consent, NAIC privacy obligations and state DOI rules give the regulator grounds to act, which then triggers the policy’s regulatory-action clause. Per the IBM Cost of a Data Breach Report 2025, 97% of organizations that suffered an AI-related breach lacked proper AI access controls. That gives the carrier a paper trail to argue the breach was foreseeable.

Which State DOIS Have Already Penalized Brokers for LLM Data Exposure?

No state DOI has publicly named LLM-specific broker penalties yet, but you’re still exposed—your broker responsibilities under existing data privacy and consumer protection statutes don’t wait for regulators to catch up with your technology adoption decisions.

Are ACORD Form Outputs From AI Tools Considered Unauthorized Reproductions?

Potentially, depending on how the AI tool is licensed and how it processes the form. ACORD’s licensing terms restrict reproduction, transmission, and field extraction of standardized form data. AI tools that ingest or output ACORD forms without licensing alignment can trigger copyright concerns and contractual violations that land on the broker’s license, not the vendor’s. Review your AI vendor’s ACORD compliance posture before any production use.

How Do I Document AI Tool Usage to Defend an E&O Claim?

Log every AI interaction with timestamps, input prompts, and outputs. Maintain client communication protocols, policy compliance checks, and training session records. Your AI usage guidelines, risk assessment frameworks, and event logging practices form your E&O defense documentation trail.

Conclusion

The brokerages binding cleanly and renewing well aren’t the ones avoiding AI. They’re the ones who built guardrails before the AI touched a client file. Hallucinations get caught by human verification. Auto-population gets caught by client sign-off. Public-LLM exposure gets caught by tool selection, not user discipline. Almost-right policy reads get caught by underwriter-grade exclusion review. Generic consultants get caught by hiring someone with a P&C license and a cybersecurity credential. None of these are technical problems. They’re workflow decisions.

Walk through your AI workflow before it backfires

PracticeForge AI builds production AI for cyber-insurance brokerages. Licensed P&C agent. CompTIA CySA+. Retired patent attorney. The five failures above are the ones we screen for in every engagement.

Or see how we work: cyber-insurance broker automation methodology.

Michael Toback is the founder of PracticeForge AI. Licensed California P&C agent (#4528883), retired California Bar and USPTO patent attorney, CompTIA CySA+, ACRM 401 Cyber Risk Management. More about Mike →